The past eighteen months have presented a defining narrative for South African debt capital markets. This journey, which began with the politically fraught delays of the 2025 National Budget, found a moment of stability in the November 2025 Medium-Term Budget Policy Statement (MTBPS), gained rhetorical momentum with the 2026 State of the Nation Address (SONA), and has now been put to its first major fiscal test with the 2026 National Budget.

By: Conway Williams, Head of Credit at Prescient Investment Management.

Throughout this period, we have witnessed a government navigating extraordinary complexity, balancing coalition politics, fiscal consolidation, and an ambitious structural reform agenda against a backdrop of sluggish growth and persistent unemployment.

As debt investors, we have been watching this journey through the specific lens of sovereign and quasi-sovereign credit quality, contingent liability risk, and the durability of the fiscal framework. The question that has been at the top of mind throughout has been simple: is the government's reform narrative translating into outcomes that structurally improve South Africa's creditworthiness and importantly, if this will translate to tangible changes going forward?

The answer, following the 2026 National Budget, is a qualified yes. But the qualifications matter enormously.

Looking Back: The 2025 MTBPS and the budget delay

When we wrote about the delay to the 2025 National Budget, we framed it as a "critical test for the GNU's cohesion." The delay, triggered by disagreements within the coalition over proposed VAT increases, was a reminder that the political architecture underpinning South Africa’s reform agenda is inherently fragile. The immediate market reaction was instructive, reflecting the market's sensitivity to any signal of policy incoherence.

The November 2025 MTBPS, however, was broadly constructive with genuinely significant milestones. For a country that has spent the better part of a decade watching debt service costs crowd out productive expenditure, the improvement in fiscal stabilisation deserved recognition. Debt service costs, which had been growing at 7.4% per annum at the time of the 2025 Budget, were now projected to grow at only 3.8% annually over the MTEF. This is a meaningful improvement that created fiscal space for investment.

However, the MTBPS also laid bare the structural constraints that continue to suppress growth. GDP growth for 2025 was revised down to 1.2%, with the medium-term outlook projecting only 1.8% average growth between 2026 and 2028. For a country with unemployment above 32% and a high debt-to-GDP ratio, this growth trajectory is simply insufficient. It is the central tension in South Africa’s credit story: the fiscal position is stabilising, but without a meaningful acceleration in growth, that stability remains fragile.

The 2026 SONA: continuity, credibility, and execution

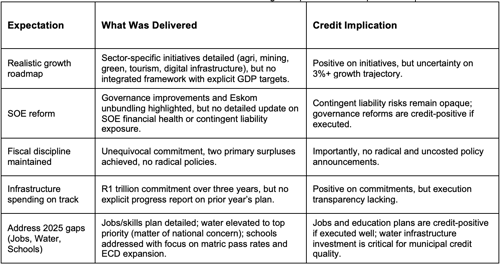

President Ramaphosa’s 2026 SONA, delivered on 12 February, was for most part constructively received. There were no major negative surprises and the commitment to fiscal discipline and structural reform was unequivocal. S&P Global’s sovereign credit rating upgrade, which preceded SONA by just days, was an external validation of the reform trajectory, citing strong tax collection and structural reform momentum.

From our post-SONA analysis, the key takeaways for debt investors were clear. The Eskom unbundling and the new SOE governance model were identified as credit-positive signals, but with an important caveat: the focus had shifted from what would be done to how and when, making implementation timelines the primary driver of SOE credit spread compression.

The R1 trillion infrastructure commitment over three years was positive on commitments, but execution transparency remained lacking.

The SONA also reinforced a theme that has become central to our investment thesis: the durability of the GNU is a key variable in the South African story. The reform continuity that has stabilised markets is contingent on the coalition holding together.

The table below summarises our assessment of the SONA against pre-address expectations:

The 2026 National Budget: execution credibility under the spotlight

Against this backdrop, the 2026 National Budget arrived at an important moment and not merely as a fiscal statement. For investors, a national budget carries a dual significance: it is simultaneously a test of a government's willingness to maintain discipline under political pressure, and a signal of its capacity to direct capital towards the structural investments that underpin long-term creditworthiness.

Infrastructure spending by government is not simply a line item; it is the foundation upon which private investment decisions are made, upon which logistics costs are determined, and upon which the productivity of the broader economy depends. A government that consistently allocates and executes on infrastructure investment demonstrates something that markets value above almost all else: durability. It signals that the reform agenda is not contingent on any single political moment, but is embedded in the machinery of the state itself.

The infrastructure story

The most substantive development is the emergence of a more sophisticated infrastructure financing architecture. The government is moving beyond simple budget allocations towards a layered model that combines public funding, PPPs, dedicated financing instruments, and institutional reform. Public-sector spending on infrastructure is projected to exceed R1 trillion over the medium term, with state-owned companies and public entities accounting for the largest share (R577.4 billion).

Several specific initiatives deserve attention:

- The Budget Facility for Infrastructure (BFI), now running quarterly bid windows, has approved R21.9 billion for five major projects, including Transnet’s vital coal and iron ore corridors.

- An infrastructure bond was successfully issued in 2025, raising R11.8 billion to support the government’s contribution to BFI-approved projects.

- The Credit Guarantee Vehicle, being developed with the World Bank, is set to become operational later in 2026 to support private investment in electricity transmission.

- The Public-Private Partnership (PPP) pipeline is growing, with 63 projects in development. The six border posts project is expected to reach financial closure this year, marking the first major PPP transaction in over five years.

South African State-Owned Entities

The 2026 Budget is in our view, notably restrained on SOEs. There are no new equity injections announced for Eskom or Transnet, and the Budget Speech does not dwell on SOE financial health in any detail. For us as investors, this restraint is itself meaningful. It signals that National Treasury is not prepared to absorb further SOE losses into the sovereign balance sheet without structural reform as a precondition.

However, it would be an overstatement to characterise this as a clean "no bailouts" position. The Budget does include a R5.8 billion special appropriation for PRASA rolling stock, and the contingency reserve makes provision for freight rail rehabilitation, a tacit acknowledgement that government financial support for the logistics sector continues in some form.

The overarching read on SOEs is this: government is making the right structural choices, but the financial risks embedded in the SOE sector remain material and only partially visible. Until these contingent liabilities are more transparently quantified and managed, they will continue to represent a ceiling on South Africa's sovereign credit improvement story.

Operation Vulindlela and Regulatory Reform

Operation Vulindlela continues to be one of the most effective delivery mechanisms for structural reform. Phase II, launched in May 2025, has expanded its mandate to include local government reform and digital transformation. The crisis in local government, with the Budget noting that 63% of municipalities are in financial distress, is a direct impediment to investment. To address this, R27.7 billion has been allocated over the medium term to a performance-linked reform for metro trading services.

The legislative pipeline is also substantive, with the Economic Regulation of Transport Act promulgated and the Water Services Amendment Bill before Parliament. These are concrete milestones that, if delivered on time, will provide the regulatory certainty that private investors require.

Conclusion - credibility and delivery

Looking back over this period, the dominant theme is one of slow, grinding progress in the right direction. The GNU has held together under considerable pressure. Fiscal discipline continues to be a key consideration. Furthermore, the reform agenda shows evidence of advancement. The 2026 National Budget reinforces this trajectory. It is a document that reflects a government that is increasingly focused on the mechanics of delivery rather than the announcement of intent. The new infrastructure financing architecture, the hardline on SOE bailouts, and the legislative progress on key reforms are all credit-positive developments.

But the risks are real. The growth outlook remains insufficient to meaningfully reduce unemployment or broaden the tax base. The contingent liabilities associated with SOEs remain opaque. The municipal debt crisis is worsening. And the durability of the GNU, which underpins the entire reform narrative, cannot be taken for granted.

For us as debt investors, our barometer has shifted. We are no longer simply looking for policy announcements. As we have previously communicated, the framework is largely in place. Our focus and analysis is now on the execution side, importantly on tangible progress against stated targets. As we wrote after SONA: credibility will be earned through delivery, not declarations.

In our view, the government has bought itself time and a degree of credibility with its consistent messaging and fiscal progress. The 2026 National Budget is a further step in the right direction. But the road to sustainable growth and lasting credit quality improvement remains long and winding. We remain cautiously optimistic and watchful.

Disclaimer

Prescient Investment Management (Pty) Ltd is an authorised Financial Services Provider (FSP 612). No action should be taken on the basis of this information without first seeking independent professional advice.

Please note that there are risks involved in buying or selling a financial product, and past performance of a financial product is not necessarily a guide to future performance. The value of financial products can increase as well as decrease over time, depending on the value of the underlying securities and market conditions. There is no guarantee in respect of capital or returns in a portfolio.

The information contained herein is provided for general information purposes only. The information and does not constitute or form part of any offer to issue or sell or any solicitation of any offer to subscribe for or purchase any particular investments. Opinions and views expressed in this document may be changed without notice at any time after publication and are, unless otherwise stated, those of the author and all rights are reserved. The information contained herein may contain proprietary information. The content of any document released or posted by Prescient is for information purposes only and is protected by copy right laws. We therefore disclaim any liability for any loss, liability, damage (whether direct or consequential) or expense of any nature whatsoever which may be suffered as a result of or which may be attributable directly or indirectly to the use of or reliance upon the information. For more information, visit www.prescient.co.za