The end of synchronised policy

For the better part of two decades, the world's major central banks have tended to move in broadly the same direction. The global financial crisis triggered coordinated easing across developed markets. When rates eventually normalised, the pandemic prompted another round of synchronised cuts. And the inflationary surge that followed saw central banks hike in near-unison. Through each of these cycles, investors could reasonably build portfolios on the assumption that the tide was moving in one direction.

Pictured: Michael Template - Quantitative Analyst at Prescient Investment Management

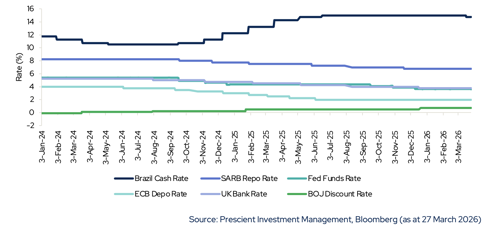

That era is now over. As we write in April 2026, the Federal Reserve holds its benchmark rate at 3.50–3.75%, the European Central Bank sits at 2.00–2.15%, the Bank of England at 3.75%, the South African Reserve Bank at 6.75%, and Brazil’s Selic rate has just been cut to 14.75% after nearly two years on hold. Each central bank faces a distinct constellation of domestic inflation dynamics, external shocks, and growth pressures — and the paths ahead are diverging further, not converging.

This divergence is not a passing phase. It reflects structural differences in fiscal positions, energy dependence, labour market dynamics, and exposure to geopolitical risk. For fixed income investors, the implication is clear: passive or static allocations are increasingly suboptimal. The opportunity set has shifted decisively in favour of active, systematic management.

Central Bank Policy Rates: Since 2024

A world of different speeds

The scale of the divergence is striking. The Fed, having cut three times in late 2025, has stalled with core PCE inflation still at 2.7% and the labour market softening. Its dot plot signals at most one further cut this year. The ECB, which had led the developed-market easing cycle with eight cuts between June 2024 and June 2025, has now pivoted sharply. President Lagarde has indicated the bank stands ready to raise rates if the inflation overshoot from the Middle East energy shock persists. Markets have moved from pricing in further ECB cuts to pricing in potential hikes. The Bank of England, confronting near-zero growth, 5.2% unemployment, and an energy-driven inflation resurgence toward 3–3.5%, faces a textbook stagflationary dilemma with no easy policy response.

In South Africa, the SARB has delivered one of the most impressive disinflation stories among emerging markets, with headline CPI reaching exactly 3.0% in February — the new target midpoint. Yet the March MPC voted unanimously to hold the repo rate at 6.75%, citing the external oil shock that now threatens to push headline inflation to 4% in the second quarter, with fuel inflation exceeding 18%. The full-year inflation forecast has been revised up to 3.7% and the SARB has modelled two conflict scenarios, both implying higher rates than previously anticipated.

Brazil illustrates the emerging-market extreme: after holding the Selic at 15% for five consecutive meetings, the central bank delivered a cautious 25 basis point cut to 14.75% in March, smaller than many expected. The broader EM picture is similarly fractured. Commodity exporters face different pressures to energy importers, fiscal positions vary enormously, and the carry available in local-currency debt ranges from low single digits to double digits. For active managers, this dispersion is the opportunity.

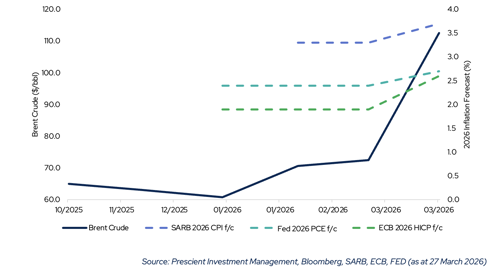

Oil price shock and inflation forecast revisions

Why divergence matters for portfolios

Divergence creates dispersion in returns, and dispersion is the raw material of active management. When all central banks are moving in the same direction, broad rate movements dominate bond returns, and a passive allocation captures most of that. But when rate paths diverge, the spread between regional outcomes widens, and the returns available to an active manager who can position across markets become meaningfully larger than what any single benchmark delivers. Over the past twelve months, the return differential between SA government bonds and US Treasuries, or between European sovereigns and UK gilts, has been substantial — dispersion that a passive global bond allocation simply averages away.

Divergence also creates asymmetric risk. The Middle East conflict has demonstrated how quickly the outlook can change and how differently a single shock affects each economy. South Africa faces a near-term inflation detour driven by fuel prices, even as longer-term inflation expectations, once accounting for the inflation-risk premium, remain well anchored around the 3% target. The UK faces a stagflationary impulse. The ECB confronts possible rate hikes after months of easing. Managing these distinct risks requires active positioning. And with credit spreads at or near generational lows across most markets, the compensation for taking credit risk is thin, making active selection not just a source of alpha, but a critical risk management tool.

A systematic framework for navigating complexity

At Prescient Investment Management, we believe the case for active fixed income management is strongest when it is underpinned by a systematic, data-driven process rather than reliant on subjective judgment. Our approach to managing the Prescient Global Income Provider Fund is built on this principle.

Research has consistently shown that asset allocation is the predominant contributor to a fund’s investment performance — far more so than individual security selection. In the credit market, picking between individual issuers requires large analyst teams to monitor a vast universe, an approach that arguably does not add value in the long run. Prescient Investment Management’s process takes a different path: we determine the optimal asset allocation positioning to deliver the best returns at the lowest risk, then compile this portfolio by investing across the global yield complex. In the global space, we gain our exposure primarily through diversified fixed income Exchange Traded Funds — buying asset classes rather than picking individual names within them — with the notable exception of US and South African Treasuries, where we invest directly. This approach provides diversified exposure across more than 15,300 underlying instruments without the concentration risk inherent in bottom-up, conviction-driven credit selection.

It is this philosophy — systematic, asset-allocation-driven, and dynamically responsive to where the global yield complex offers the best risk-adjusted opportunities — that underpins the Prescient Global Income Provider Fund and, we believe, represents the right framework for navigating the environment ahead.

Looking ahead

The near-term outlook is dominated by the Middle East conflict. If it is resolved quickly, the inflationary impulse fades and central banks regain the ability to ease. If it persists, the divergence intensifies. But regardless of the geopolitical outcome, the structural case for divergence endures: the US fiscal trajectory remains unsustainable, Europe’s growth model is being reshaped by defence spending and energy transition, South Africa’s new 3% inflation target is a genuine regime change, and emerging markets are navigating idiosyncratic dynamics that bear little resemblance to developed-market patterns.

The simple playbook of the past decade — buy duration, wait for rate cuts, collect carry — no longer works uniformly. Income has returned to fixed income after years of famine, and real yields in several markets are genuinely attractive. But capturing these opportunities while managing the risks of heightened uncertainty requires systematic, data-driven rigour that can process the full complexity of the global yield landscape.

At Prescient Investment Management, that is the approach we take. The era of synchronised policy is over. What follows demands a different kind of fixed income management.

Disclaimer:

Prescient Investment Management (Pty) Ltd is an authorised Financial Services Provider (FSP 612).

Collective Investment Schemes in Securities (CIS) should be considered as medium-to-long-term investments. The value may go up as well as down and past performance is not necessarily a guide to future performance. CISs are traded at the ruling price and can engage in scrip lending and borrowing. A schedule of fees, charges and maximum commissions is available on request from the Manager. There is no guarantee in respect of capital or returns in a portfolio. A CIS may be closed to new investors in order for it to be managed more efficiently in accordance with its mandate. Performance has been calculated using net NAV to NAV numbers with income reinvested. Prescient Management Company (RF) (Pty) Ltd is registered and approved under the Collective Investment Schemes Control Act (No.45 of 2002). Prescient is a member of the Association for Savings and Investments South Africa. The Prescient Global Income Provider Fund registered and approved under section 65 of the Collective Investment Schemes Control Act 45 of 2002.

Please note there are risks involved in buying or selling a financial product, and past performance of a financial product is not necessarily a guide to future performance. The value of financial products can increase as well as decrease over time, depending on the value of the underlying securities and market conditions. There is no guarantee in respect of capital or returns in a portfolio.

This document is for information purposes only and does not constitute or form part of any offer to issue or sell or any solicitation of any offer to subscribe for or purchase any particular investments. Opinions expressed in this document may be changed without notice at any time after publication. We therefore disclaim any liability for any loss, liability, damage (whether direct or consequential) or expense of any nature whatsoever which may be suffered as a result of or which may be attributable directly or indirectly to the use of or reliance upon the information. For more information visit www.prescient.co.za