Prescient Investment Management’s approach has always been to investigate a story before it becomes a fact, rather than following a narrative that might make sense but may not be true. How many times have you heard a portfolio manager talk about how their “rand hedge” stocks provided a good buffer in a weakening rand environment?

Pictured: Rupert Hare - Head of Multi-Asset at Prescient Investment Management

The term “rand hedge” is a classic within stock picking circles. It’s usually seen as a stock which serves as a good off setter (contributes positively to performance) when the rand blows out due to the strong reliance on offshore earnings.

Their counterparts, “SA Inc” shares, gives reference to shares which earn most of their revenues in rands - so any rand weakness has no material impact on their profit margins from exports but may be a sign of other problems in the economy.

There is no doubt that a company that earns most of its revenues offshore should benefit from those revenues coming into the country at an exchange rate of R19 instead of R16, but what impact does that have on the share price?

This is the key disconnect that often happens between a fundamental analyst dissecting the balance sheet versus a quantitative analyst who checks for impacts of a factor on a share price. Spoiler alert – it’s not what you think!

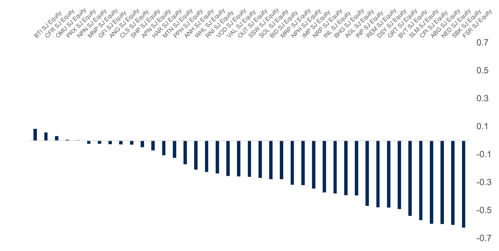

Looking at the correlations of Top40 stocks versus movements in the rand we see that banks and insurers (the classic “SA Inc” companies) do exhibit a strong relationship to the rand – in their case when the rand weakens their share prices tend to fall. But what is interesting is that contrary to balance sheet logic, there aren’t any shares on the flip side of that coin which show a significant and reliable price rally when the rand weakens.

At Prescient Investment Management, we rather trade the fact than the narrative, so for our Prescient Income Fund looking to gain some offshore currency exposure to hedge against rand weakness, rather than buying rand hedge property counters or stocks we’ll simply by a USDZAR futures contract. The future isn’t linked to the rand/dollar via some sort of loose relationship that works sometimes and sometimes not – instead its contractually linked to the exchange rate – no questions asked and no doubts had.

Conversely our Prescient Balanced Fund, which already has significant offshore exposure, hedges back a portion of that exchange rate risk into rands using USDZAR forward contracts, avoiding a scenario like last year where funds with large offshore exposures got knocked by a strong rand rally. At the same time, it doesn’t miss out on rand depreciation, it earns the carry rate.

The key takeaway here is that everything that is taken as fact should be investigated before being regurgitated as fact. Rand hedge stocks that gain when the rand sells off may have improved balance sheets, but their share prices don’t react with any degree of certainty. The same applies to stylised facts like “paying high fees is worth it for the performance”, “our funds are not benchmark cognisant” or “picking a few global single stock names like Apple or Nvidea gives broad-based global exposure”.

Asset management is as much a marketing game as it is a performance one, and investors often subconsciously place far too much weight on the former than the latter.

Disclaimer

Prescient Investment Management (Pty) Ltd is an authorised Financial Services Provider (FSP 612).

Collective Investment Schemes in Securities (CIS) should be considered medium to long-term investments. The value may go up as well as down and past performance is not necessarily a guide to future performance. There are no guarantees. Please note that there are risks involved in buying or selling any financial product. Prescient Management Company (RF) (Pty) Ltd is approved under the Collective Investment Schemes Control Act (No.45 of 2002). For any additional information please go to www.prescient.co.za.