Positioning for a Growth Slowdown, Not a Fiscal Crisis

Prescient Investment Management remains constructive on the 5-year US Treasury. At current yield levels, the instrument offers attractive risk-adjusted returns in a scenario of slowing US growth. While concerns around debt levels, dollar debasement, and fiscal sustainability are widely cited, these are long-term structural risks unlikely to dominate over a 5-year horizon. The 5-year Treasury is primarily a policy-cycle instrument, driven by Federal Reserve easing expectations and the growth outlook — not by long-term debt dynamics.

Pictured: Henk Kotze - Head of Cash and Income at Prescient Investment Management

The 5-Year Treasury Prices the Cycle, Not Structural Debt Risks

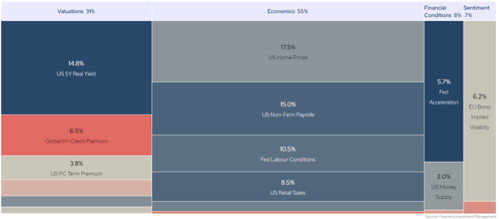

The 5-year point on the US Treasury curve is, by its nature, a cyclical instrument. Its yield reflects the market’s expectation of the Federal Reserve’s policy path over the next three to five years, prevailing inflation expectations, and a modest term premium. It is not a referendum on 20-year fiscal trajectories, reserve currency dynamics, or long-term debt sustainability. Investors who conflate these two time horizons risk misidentifying both the risk and the opportunity. We are not expressing a view on US fiscal policy — we are positioning for the next easing cycle. The below gives a clear depiction of our constructive view as well as what factors are driving this view. The blue tiles under the economics factors shows that we see the slow down in growth as being bullish for the 5-year part of the yield curve.

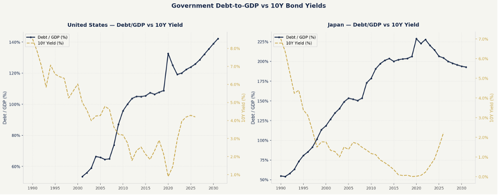

High Government Debt Does Not Automatically Lead to Higher Yields

The assumption that rising debt must push yields higher is not supported by historical evidence. Japan is the clearest illustration: government debt has exceeded 250% of GDP for over a decade, yet 10-year yields remained near zero throughout. In the US, the debt surge of 2020–2021 coincided with a collapse in yields as the growth shock overwhelmed fiscal concerns. Across the Eurozone, core sovereign yields fell during periods of fiscal stress as capital rotated toward safety. The mechanism is consistent: when growth slows, investors seek safe assets and Treasuries rally. Debt levels become a yield driver primarily when inflation is rising and central banks are forced to respond — not during slowdowns where disinflationary forces dominate.

Safe-Haven Demand Strengthens in Growth Shocks

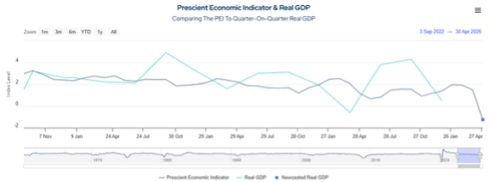

In a US growth slowdown scenario, the mechanics are straightforward: risk assets sell off, global liquidity tightens, and capital flows toward US Treasuries. This demand is structural, not discretionary. Treasuries remain the world’s primary risk-free collateral, central to global repo markets and derivatives clearing, and a mandatory component of bank liquidity buffers under HQLA requirements. Even as central banks modestly diversify reserve holdings, their operational reliance on Treasuries as collateral is unchanged. In stress scenarios, demand for US government bonds increases — it does not diminish. The chart below shows our current nowcast of US growth using our Prescient Economic Indicator.

Dollar Debasement Requires Sustained Inflation — Not Our Base Case

Currency debasement, in any meaningful sense, requires persistent inflation above nominal yields and an erosion of central bank credibility. Current dynamics point in the opposite direction: structural goods disinflation is underway, wage growth is moderating, financial conditions remain restrictive, and long-term inflation expectations are anchored. The 5-year breakeven inflation rate — the market’s implied inflation expectation — remains contained, signalling that investors do not anticipate the sustained inflationary pressure that debasement narratives require. Without that foundation, the argument lacks a credible transmission mechanism. The below 5-year Inflation Swap shows clearly market inflation expectations has not become debased, even in the current market environment.

Fiscal Dominance Is Not the Base Case

The debasement narrative rests on the assumption that the Federal Reserve will ultimately monetise government debt — a condition known as fiscal dominance. The evidence does not support this. Real policy rates remain positive, quantitative tightening continues, and the Fed has maintained a restrictive stance despite elevated debt levels and political pressure. This is consistent with policy independence, not fiscal capture. Without fiscal dominance, high debt does not automatically translate into inflation or structurally higher yields. The Fed has both the tools and, thus far, the institutional will to prevent it.

Why the 5-Year Point Is the Sweet Spot

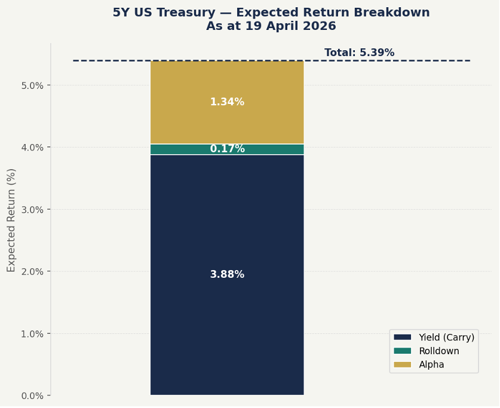

Relative to longer duration, the 5-year sector carries lower exposure to fiscal term premium risk — the compensation investors demand for holding long-dated bonds subject to uncertain long-run fiscal outcomes. It is also more responsive to Fed easing, delivering better risk-adjusted duration in a cutting cycle. Relative to the 2-year, the 5-year captures the full arc of an easing cycle rather than just the initial moves, and is materially less sensitive to near-term data volatility. For investors positioned for a slowdown, the 5-year sector provides the most efficient expression of that view. The below breakdown of our 12-month expected return for the 5-year sector shows how we expect the compression in yields to add to the total return.

Balanced View: What Would Challenge the Bull Case?

A disciplined systematic investment process requires explicit acknowledgement of the risks to any base case. The constructive view on 5-year Treasuries would be challenged by a re-acceleration of inflation, a sustained rise in inflation expectations, a loss of Federal Reserve credibility, or a structural repricing of the term premium driven by deteriorating fiscal dynamics. These risks are not dismissed — they are actively monitored. The act of articulating them reinforces conviction in the base case: none of these conditions are present in the current environment.

Conclusion: A Cyclical Opportunity Within a Structural Debate

The debasement argument is fundamentally a long-term structural concern. The 5-year Treasury is fundamentally a cyclical instrument. These two realities operate on different time horizons, and conflating them leads to misplaced caution. If growth slows and inflation moderates — our base case — the 5-year yield has room to decline materially, regardless of the debt stock. History is clear: in a slowdown, yields fall. Debt or no debt.

Disclaimer

Prescient Investment Management (Pty) Ltd is an authorised Financial Services Provider (FSP 612).

The information contained herein is provided for general information and marketing purposes only and does not constitute financial, investment, legal, tax or other advice. This document has not been prepared in accordance with the legal requirements applicable to the rendering of advice and does not take into account any investor’s objectives, financial situation or needs. Any investment is subject to risk, including the risk of capital loss. Past performance is not a reliable indicator of future results. Forecasts, forward-looking statements and any targets are not guarantees and are provided for illustrative purposes only. While care has been taken to ensure the information is accurate, Prescient Investment Management (Pty) Ltd makes no representation or warranty as to the accuracy, completeness or correctness of the information and accepts no liability for any loss, damage, cost or expense (whether direct, indirect, special or consequential) arising from the use of, or reliance on, this information. Opinions and views expressed are those of the author as at the date of publication and may change without notice. This document is not an offer to issue or sell or a solicitation of any offer to subscribe for or purchase any investments. For more information visit www.prescient.co.za.